Port inventories’ nightmare to haunt Capes?

08.03.2019High iron ore inventories at Chinese ports and looming uncertainty in the global economy are threatening the demand for Capesizes.

We believe demand for Capesizes in 2019 will be proportional to iron ore inventories at Chinese ports. Even though China’s steel production will rise in 2019, a further drawdown in iron ore inventories could adversely affect the demand for dry bulk vessels.

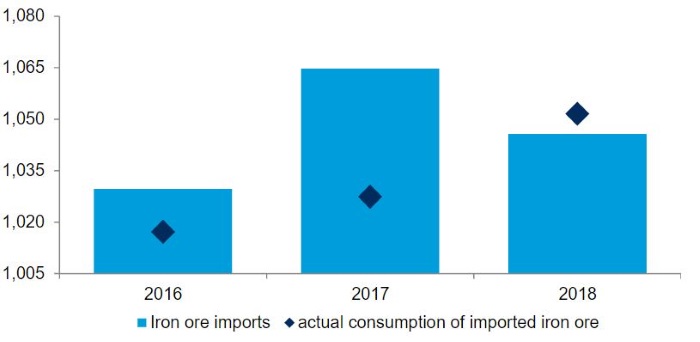

In 2018, China’s iron ore imports fell 1.8% year on year even though the country’s steel production increased at a robust pace during the same period. While the country’s consumption of imported iron ore was indeed higher in 2018 compared with 2017, imports declined as steel mills preferred to drawdown on port inventories.

This leads to an obvious question: How will China’s inventory story unfold in the near term? In this respect Drewry believes two opposite forces are working in the background

Firstly the Chinese government’s push for infrastructure and easing in monetary policy will continue to drive up the demand for steel in the country. Also, since the government is still committed to the clean air initiative, the country’s steel sector will remain under scrutiny for emissions. In turn this will support the demand for high quality ore, primarily met by imports. This will be positive for the dry bulk sector and will help underpin imports.

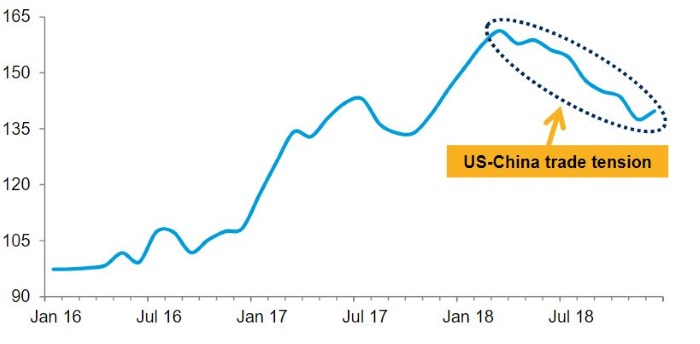

That said we can also see that the probability of low inventories is very high as trade friction with the US will continue for some time before tensions are fully abated. Meanwhile, China’s economy grew by 6.6% in 2018, which is the slowest growth in the last 28 years, and furthermore the IMF projects growth to drop to 6.2% in 2019 and 2020. In this scenario sentiment will remain weak and steel mills will remain cautious on future steel demand, thereby compelling millers to continue drawing down on port inventories.

In 2018, average quarter-on-quarter decline in inventories was about seven million tonnes and we assume that in first-half 2019 inventories will keep declining at the same pace. Furthermore, most of the decline in inventories will be a substitution for imports from Brazil, especially as Brazilian export capacity has been reduced due to the recent dam burst. In short, we think the prospect of strong iron ore import growth in China in 2019 is low and for that reason Capesize demand is under threat.

Source:hellenicshippingnews.com