The Good, the Bad, and the Ugly

14.05.2018Our COO Adrian Economakis presented recently on the ‘The Strength of Recovery in the Shipping Markets’. Using VV data we summarise the Good, the Bad and the Ugly of the shipping markets.

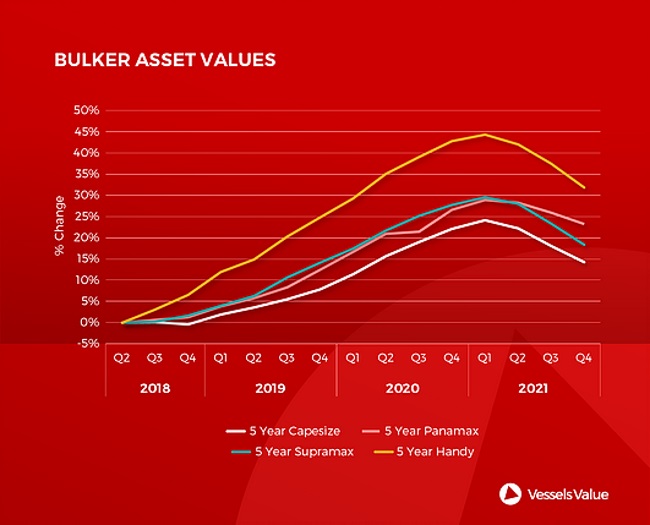

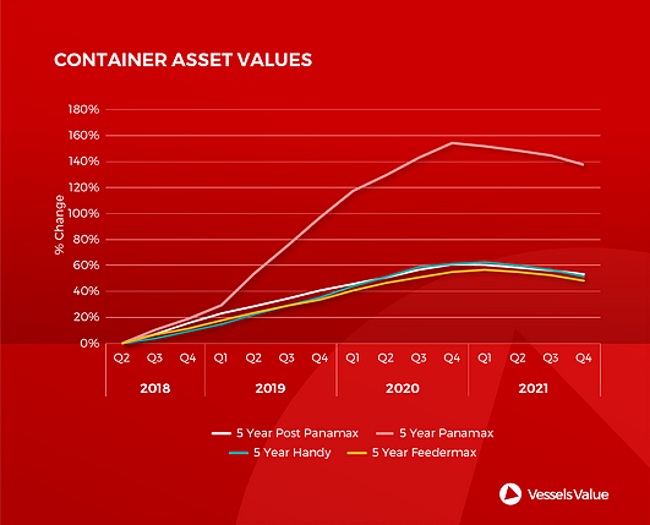

THE GOOD

Two years ago the Bulker and Container markets were in a sorry state, fast forward to today and the market has significantly improved, with upside remaining. Over the past twelve months Panamax container ships have seen a rebound in asset values of about 40 pc for a five year old ship over the past year . In addition, earnings are above operating costs. There is a lot of positive sentiment and we expect Bulkers and Container values to continue this pattern in the next 2-3 years.

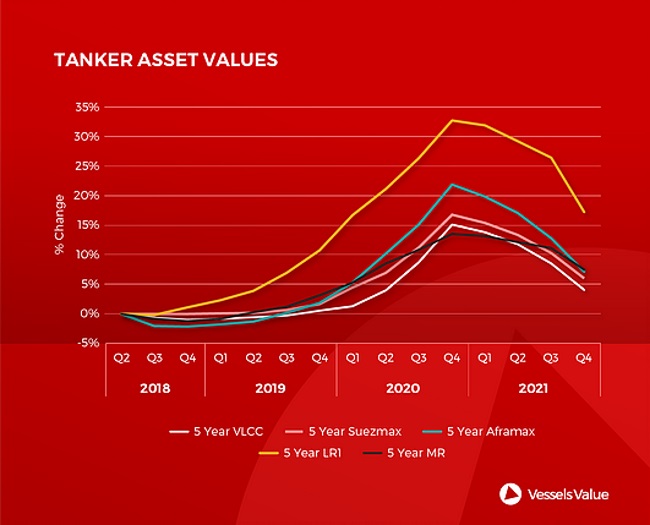

THE BAD

Tanker earnings are low, especially for the large crude tankers. Small clean tankers are doing somewhat better but remain depressed. The general improvement in the shipping market has seen asset values for Tankers up by 10% and smaller Tankers up 20% from last year despite the weak spot markets. The outlook for prime aged asset values looks positive as we appear to be at the bottom of the market.

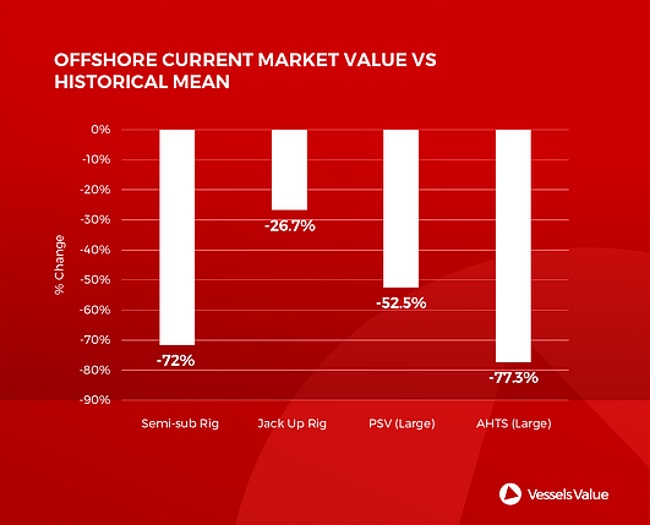

THE UGLY

The Offshore industry has seen a 70% decrease in values in the past two years, this is due to oil prices coming down from $130 USD in 2014/2015 to $30-$40 USD. A recovery in oil prices has begun, although it takes time for the oil companies to restart their exploration. Offshore is still saturated with low value commodity type OSV and AHTS, it is expected that the values will remain low over the next few years. It is not all bad for the Offshore industry with areas of interest such as Diver Support Vessels, Offshore Support Vessels and accommodation vessels that are still being used to maintain existing structures.

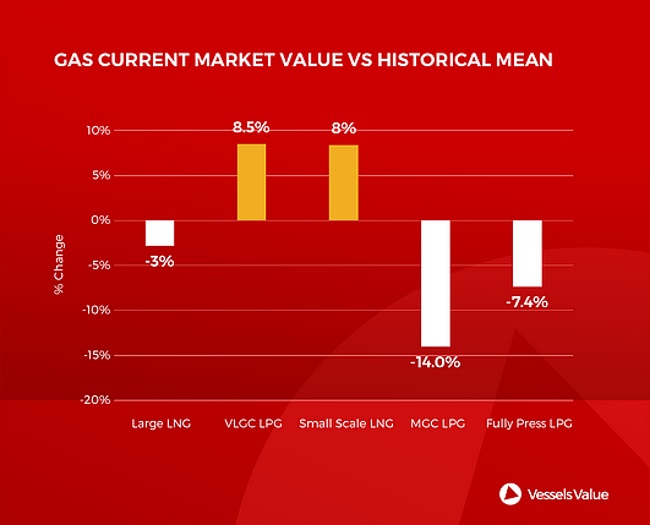

GAS

Gas does not fit into the good, the bad, or the ugly categories. Values have dropped a little but it’s not particularly going up and down quickly. Demand is good and growing, however while the market was too good, too many vessels were built and there were restrictions on the market.

Source: www.hellenicshippingnews.com